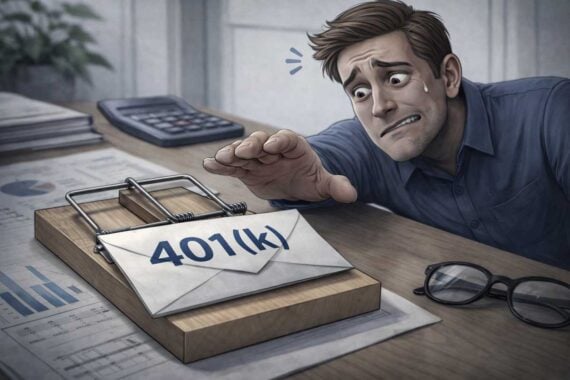

More Americans are treating their 401(k) like an emergency fund … and not by choice.

A record 6% of workers took hardship withdrawals in 2025, according to new Vanguard data, a sign that when unexpected expenses hit, many households don’t have anywhere else to turn. The most common reasons feel painfully familiar: avoiding eviction, covering medical bills, paying for tuition, or handling urgent home repairs.

The problem is what happens next. A 401(k) withdrawal doesn’t just solve a short-term issue — it quietly creates a long-term one. That money loses years (or decades) of compound growth, and, in some cases, comes with taxes and penalties that make the situation even more expensive.

Financial pressure is real. But before dipping into retirement savings, there are other ways to bridge the gap without derailing your future.

Start With Your Employer Benefits

Many people skip the simplest option because they don’t realize it exists. Some employers offer paycheck advances, emergency assistance programs, or short-term loans tied to retirement plans.

A 401(k) loan, for example, can be a better option than a hardship withdrawal. You’re borrowing from yourself and paying the money back — with interest — into your own account. It’s not risk-free (leaving your job can accelerate repayment), but it avoids permanently draining your savings.

Negotiate the Bill Before You Pay It

Medical bills, in particular, are often more flexible than they look. Providers may offer payment plans, discounts for paying in cash, or even financial assistance programs.

The same goes for housing. If you’re facing eviction or falling behind, landlords and lenders are often more willing to work out a plan than lose a tenant or deal with foreclosure costs.

It’s not always comfortable, but asking can buy time — and time is often what prevents a financial spiral.

Cut or Pause Contributions — Temporarily

This one feels counterintuitive, but it can be a smarter move.

If you’re facing a short-term financial crunch, temporarily reducing or pausing 401(k) contributions can free up cash flow without triggering taxes or penalties. Once things stabilize, contributions can resume.

It’s not ideal, especially if it means missing out on an employer match, but it’s still less damaging than withdrawing funds entirely.

Look Into Hardship Alternatives

Before touching your 401(k), it’s worth checking for:

- Local or state emergency assistance programs

- Nonprofit aid for housing, utilities, or medical bills

- Payment deferrals or forbearance options on loans

These options often exist specifically to prevent people from draining long-term savings during short-term crises.

More From Cheapism

- ‘It’s Rough Out There’: A Record Number of Americans Are Tapping Their Retirement Savings Early — More Americans than ever before are feeling so much financial pressure, they’re tapping into their retirement savings early.

- No 401(k)? Trump Says He Has a New Retirement Fix — If you don’t have a 401k, the president proposes a solution.

- Financial Experts Share 25 Ways Your Money Disappears Into the Void — There are so many ways to lose money, and financial experts call these things out as the key culprits.