That sinking feeling when you check your bank account and your paycheck is already gone? That’s what most of us deal with every month. On the flip side, people are sick of apps and budgeting tools that promise clarity but just add noise. That’s probably why a 120-year-old Japanese method called Kakeibo is showing up again online.

Studies show that most Americans know they’re overspending, with 74% saying they have a problem and one third admitting they bought something they knew they couldn’t afford. In another survey, 42% said they treat themselves every month, and 21% admitted to non-essential spending at least weekly. Triggers are your usual boredom and stress (20%).

To combat this overspending, people are turning to a budgeting style that resembles journaling. Read on for more about the Kakeibo method.

What Is Kakeibo?

Kakeibo literally translates to “household financial ledger” and encourages you to plan how much you’ll save, track what you spend, and then ask why you are spending.

The method was invented in Japan back in 1904 by Hani Motoko, Japan’s first female journalist, in a women’s magazine aimed at helping households manage finance. In its early form, it asked homemakers to record income, fixed costs, savings target, and variable spending. Over time, people have adapted it outside Japan.

Nowadays, it’s getting a lot of attention for its simplicity, and has gone viral among savvy savers of the internet.

How Does Kakeibo Work?

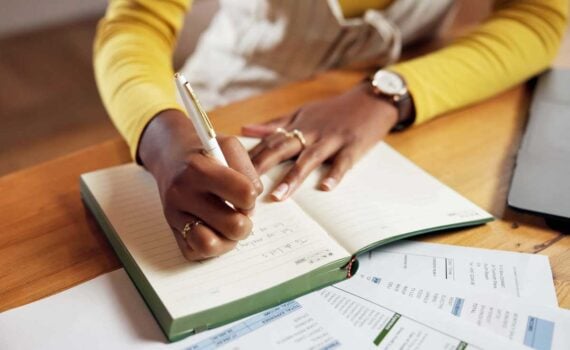

Kakeibo is essentially a monthly money journal-meets-envelope budgeting technique. You start by writing down your income, your recurring bills, and your savings goal. You use a notebook and a pen, not an app. Each time you spend, you record the amount, date, reason. At the end of the month, you total it all up and see what really happened.

The method is not about being strict or counting every cent forever, but keeping a log and discovering spending patterns. When you write things down, you start seeing patterns you didn’t notice before.

Step 1: Write Down What You Have

The best way to start is write down your income after taxes and necessary expenses, like rent, utilities, insurance, and other recurring payments. Once that’s out of the way, what’s left is the money you actually get to make decisions about.

Step 2: Set a Savings Goal

Decide how much of that leftover cash you want to hang onto — what you’ll actually move into savings before anything else happens. Kakeibo works best when you treat saving like a non-negotiable, not something that might happen if the month goes well.

Step 3: Record Every Expense

As you go through the month, write down every purchase. Every time you spend, write down the date, the amount, what it was for, and where it fits. Use a pen if you can. When you write by hand, your brain actually processes the action.

Trending on Cheapism

Step 4: Put It in the Right Box

Every purchase lands in what the method calls a “box:”

- Needs cover the basics: rent, food, transport.

- Wants are comfort stuff — takeout, shopping, entertainment.

- Culture is anything that feeds your brain: books, hobbies, streaming, concerts.

- Unexpected is the curveball category — car repairs, gifts, the stuff you didn’t plan for.

When you review the month, you’ll see what category eats the most of your paycheck — and that’s where the real insight happens.

Step 5: Look Back and Adjust

When the month ends, go over what happened. Add it up, compare it to what you planned, and see what doesn’t line up. Don’t overthink it. Maybe your rent’s fine but your grocery spending doubled. Maybe you bought things out of stress. Whatever it is, you’ll see it. And once you see it, you can’t unsee it. That’s where it starts to change.

What People Think About It

As with everything on the internet, some people are thrilled to have discovered the method online, while others fall into the “whatever, this is nothing new” category.

“I’ve been using a Kakeibo budget for about 7 or 8 years,” said one Redditor. “My wife came on board about April 2020. We love both the intentionality and the simplicity. We don’t have to “rob” from one category to another because we’ve overspent on something. We have our weekly budget amount and just track against that. Absolutely simple and zero fighting over money or spending.”

Another said, “It makes me far more aware and intentional. I’ve traced all my recent purchases and considered them, if not returned them outright.”

But someone argued it’s basically a repackaged envelope method: “I mean, it’s just the envelope method with a fancy Japanese name and boxes instead of envelopes.”

Sign up for our newsletter

More Budgeting Content:

- 11 Budgeting Mistakes That Could Cost You — Avoid these mistakes so that you actually can cut back on spending.

- 10 Mistakes to Avoid When Creating a Household Budget — These tips will help keep you from sabotaging your own plans and financial wellness.

- Low-Stress Ways to Save for Life’s Unexpected Expenses — Read on for suggestions on how to grow your emergency fund and tweak finances to create a cushion with as little pain as possible.