Sometimes you do things that seem like they’ll save you money, like buying ultra cheap items or stocking up on things in bulk. Turns out, these budgeting mistakes can actually cost you in the long run. Avoid these misshaps so you can truly cut back on spending.

Buying Cheaply Made Products

That alarm clock on Temu is just $.99! What a great deal, you think. Only, it breaks after three days of use.

Not everything cheap is quality-made. Imagine what kind of materials and labor the company could put into a $.99 clock. Not much.

When you buy cheap products that fall apart, you end up spending more to replace them. You’re better off investing a little more to get a well-made product that will last for years.

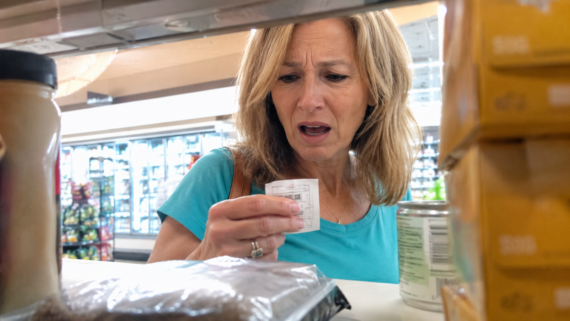

Buying Perishable Groceries in Bulk

Warehouse stores like Costco can help you save money by selling products in bulk, but if you can’t use all of what you buy before it goes bad, you’re throwing money down the drain.

If you can’t consume, for example, five pounds of bananas before they turn black, consider splitting the purchase with a friend or peeling and freezing the extras to be thrown into smoothies later.

And remember: It’s not only warehouse stores that offer great deals. By paying attention to grocery store flyers, you can find produce and meat on sale. Buy as much as you can consume, and you’ll save without wasting food.

Not Thinking About Where You Shop

Speaking of paying attention to grocery store sales … are you the kind of person who just shops at the most convenient store, or do you shop around for the best deals?

Yes, it may mean making multiple grocery store runs, but buying what’s on sale at different stores is a great cost-saving strategy. Otherwise, you end up kicking yourself when you see you could have paid half of what you paid for something simply by being strategic about your shopping.

Financing Larger Purchases

So you’re buying a fridge or other high-ticket purchase and you’re considering taking advantage of the financing offer the store is promoting. Paying $50 a month sounds a lot better than paying $800 all at once, right?

Wrong.

Financing purchases means you pay interest and fees in addition to the purchase price. So that $800 refrigerator could end up costing a grand if you take months or years to pay it off. Better to save up your money and pay it all at once.

Ignoring Sales Seasons

You want to buy outdoor furniture, so you buy it at the start of the summer. At the end of the summer, you see sales at all the stores with prices slashed by 50% or more. If you’d only waited, you could have saved hundreds of dollars.

The same goes for clothes. Wait until the end of the season to snag shirts, coats, swimsuits, and pants for a fraction of their price at the start of the season.

If you love your holiday decor, wait until after Christmas, Easter, or Halloween to get cute things for pennies on the dollar.

Trending on Cheapism

Not Having a Budget

You feel like you have a handle on your spending, yet you never seem to have any extra money at the end of the month. If you don’t have a budget, you’ll never fully know what you’re spending, nor will you be able to save money.

Use budgeting software to list your monthly expenses, including rent or mortgage payments, groceries, utilities, car payments, and discretionary expenses. If you want to have money for something special, like a vacation or wedding, use your budget to see where you can cut costs and set money aside.

Not Reviewing Expenses

You signed up for that horror channel subscription service months ago but haven’t used it in ages. Essentially, you’re wasting money.

Another perk of having a budget is that you can keep a closer eye on your expenses and eliminate those that you don’t need. Make a point to review your bank statements every month to ensure that all your expenses are the ones you need. For any subscriptions or memberships you’re not using, cancel them and save the money.

Paying Only the Minimum on Your Credit Card

If your monthly credit card statement tells you that you only need to pay $25, you do so. The problem is that you’re rapidly accumulating interest expenses, so anything you charge on that credit card ends up costing you a whole lot more.

For example, if you charge $1,000 on your card, which has 25% interest, and make 12 equal payments over a year, you’ll end up paying $1,200 in total! Why give the credit card company your hard-earned money?

Sign up for our newsletter

Impulse Shopping

Nothing good ever comes of buying things you don’t need, right? Maybe you go to the grocery store when you’re hungry or the mall when you’re stressed. Either way, you come home loaded with bags of stuff you don’t need and can’t afford.

If you’re a millionaire, this isn’t a problem. If you’re not, only go shopping with a list or a firm idea of what you’re out to purchase. That way you don’t spend more than you intended.

Not Having a Savings Account

You tell yourself that if you want to save money, you’ll do it in your primary checking account. But somehow, that money always seems to disappear.

Not having a savings account not only makes it harder to save money, but it also means you’re missing out on the interest one can provide.

You can automatically transfer money to your savings account each month without having to think about it. Once it’s there, you’re less likely to spend it. And while your money sits in a savings account, it earns interest, so you make more while doing less.

Not Being Smart with Credit Cards

While it’s always better to pay for expenses with money you have today rather than with credit, it can be helpful to have a credit card. But the kind of credit card also matters.

There are credit cards with rewards programs that give you points for every purchase. These points can be used for cash back, travel, and other perks. If you’re going to charge expenses, why not get something out of it?

Especially if you’re making larger purchases, like putting a new roof on your home, charging these expenses (and having a plan to pay them off) can actually pay you!

Ignoring Tax Withholding and Take-Home Pay

When planning a budget, use your net (take-home) income after taxes and other payroll deductions — not your gross salary. Budgeting based on your gross pay can make you overestimate what you actually have to spend, leading to shortfalls later in the month.

Not Building a Tiered Savings System

Many resources recommend just having a single savings account, but you can take it a step further by setting up multiple savings “buckets” for different purposes. For instance, you might keep one bucket for an emergency fund that covers three to six months of essential expenses, another for short-term goals like vacations or holiday gifts, and a third for long-term goals such as a down payment or retirement.

Keeping these funds separate makes it less tempting to pull money from the wrong place and gives you a clearer picture of how you’re progressing toward each specific goal.

Not Keeping Track of Small Purchases

Tiny purchases — like daily coffee, quick snacks, or small subscription add-ons — can silently add up and derail your budget if ignored. Regularly tracking even these micro expenses keeps you aware of where money leaks occur and gives more accurate spending data.

More From Cheapism

- Financial Experts Share 25 Ways Your Money Disappears Into the Void — Even small costs like unused subscriptions, daily coffees, and overlooked fees can quietly drain your wallet if you don’t plug the leaks.

- Things You Should Avoid Buying in January — and Why — January sales can be misleading, and holding off on items like winter gear or mattresses often leads to much deeper discounts later in the year.

- 17 Easy Hacks to Help You Save Money Every Day — Small, practical changes to your daily routine can add up to real savings without forcing you to overhaul your lifestyle.