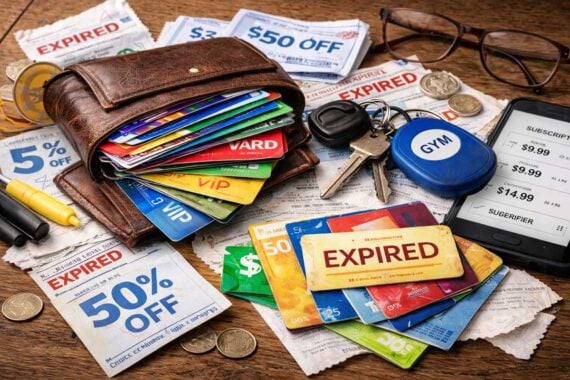

You probably don’t think twice about what’s sitting in your wallet, purse, or everyday bag. But some of the items you carry around daily can subtly chip away at your finances — and a few may even cost you money without you realizing it, encouraging impulse purchases, adding interest charges, or making it harder to keep track of your spending.

Sometimes the cost isn’t obvious. It’s not a big bill or a dramatic expense — it’s small habits, convenience fees, and psychological triggers that add up over time. Here are 10 things you might be carrying that are quietly costing you more than you realize.

Store Credit Cards You Rarely Use

That instant discount at checkout can be tempting, but store credit cards often come with sky-high interest rates — sometimes well above standard credit cards. If you carry a balance even once, the interest can cancel out any initial savings. Plus, simply having the card in your wallet makes it easier to justify impulse purchases at that retailer. If you only shop there once or twice a year, the temptation and potential interest charges may outweigh the perks.

Untracked Cash

Paying with cash can feel like a smart budgeting move — but only if you’re actually tracking it. When you aren’t logging those small cash purchases, it becomes easy to underestimate how much you’re spending. A few $5 or $10 transactions here and there can quietly turn into hundreds of dollars a month. Unlike card purchases, cash doesn’t leave a digital trail, which makes it harder to spot patterns or overspending.

Old or Forgotten Gift Cards

Unused gift cards are essentially prepaid money sitting idle. If you forget about them, misplace them, or let them sit for years, that’s money you’ve already spent but never actually used. Some cards also charge inactivity fees after long periods. Keeping them buried in your wallet without a plan to use them means you’re not getting the full value you paid for.

Too Many Membership Cards

Loyalty programs promise points, discounts, and “exclusive” deals — but they’re also designed to increase how often you shop. Carrying multiple membership cards can subtly influence your behavior, encouraging you to buy more frequently just to maximize rewards. In many cases, you may end up spending more than you save simply because you don’t want the points to “go to waste.”

Multiple Credit Cards

Having several credit cards isn’t inherently bad — but carrying all of them increases temptation. More available credit can make large purchases feel manageable, even if they strain your budget later. You may also be juggling multiple billing cycles, annual fees, or rewards programs, which increases the risk of missing a payment. Even one late fee or interest charge can quietly undo months of careful spending.

Trending on Cheapism

A Gym Membership Tag You Rarely Use

If you’re carrying the key tag but not going regularly, you’re essentially paying a monthly fee for good intentions. Many people hold onto memberships thinking they’ll “start next week,” while automatic charges continue month after month. If you’re not consistently using the gym, it may be time to reconsider whether the cost aligns with your actual habits.

Coupons That Push You to Spend

Discounts can feel like savings, but only if the purchase was already planned. Carrying coupons may encourage you to buy items simply because they’re on sale. Retailers rely on this psychology — a small discount can make spending feel justified, even if it wasn’t in your budget. In the end, you may spend more than you intended.

Easy Access to Delivery and Shopping Apps

Having shopping and food delivery apps logged in and ready to use removes friction from spending. When ordering dinner or buying household items takes just a few taps, it’s easier to justify convenience fees, service charges, and tips. Those small add-ons can significantly inflate the true cost of purchases over time.

Sign up for our newsletter

Buy Now, Pay Later Accounts

Installment payment services make purchases feel smaller and more manageable by splitting them into chunks. But stacking multiple “small” payments across different platforms can create a hidden monthly burden. It’s easy to lose track of how many payments are still pending — and missing one can trigger late fees or affect your credit.

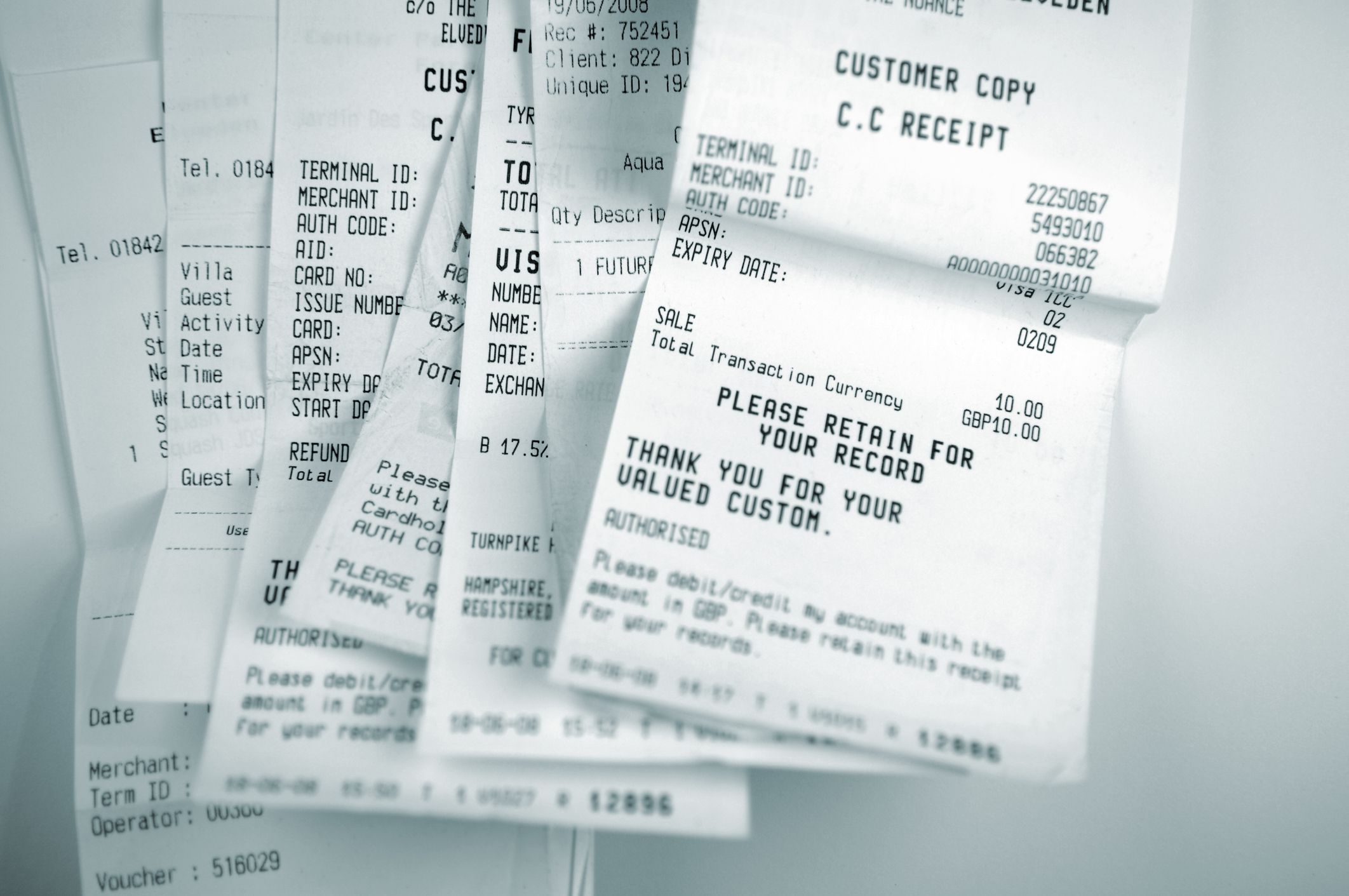

Receipts You Never Review

If you’re tossing receipts into your wallet but never checking them, you could be overlooking overcharges, incorrect prices, or missed return windows. Small billing errors add up, especially if they happen frequently. Taking a few minutes to review receipts can prevent you from losing money on mistakes you didn’t even notice.

More From Cheapism

- ‘Our Electric Bill Is Eating Us Alive’: Electricity Bills Are Rising, No Matter How Much We Try to Save — If your monthly utility bill feels shockingly high even when you’re cutting usage, inflation, aging infrastructure, and other hidden forces might be silently blowing your budget.

- Sneaky Dealer Fees You Should Absolutely Refuse When Buying a Car — Don’t hand over extra cash at the dealership: several high-markup “add-ons” are optional and saying no can save you hundreds or more before you sign.

- ‘It’s Just Not Worth It Anymore’: How to Scratch the Takeout Itch Without Spending the Money — Takeout bills leaving you cringing? Try smart swaps and home-friendly hacks that satisfy cravings without draining your wallet.